Models: Wuling Mini EV #1 in April

Registrations were up for an impressive 249% last month, to some 392,000 units, the 4th best month ever, with BEVs jumping 235%, to some 251,000 units, so we might be seeing the plugin market hit 5 million units this year.

These impressive results this year kept the 2021 PEV share to 5.7% (3.7% BEV), which is already significantly above the 4% of last year, and expect it to continue growing throughout the year, to a large single digit number, as Disruption (eg, two digit market shares) on a global level is looking set to happen in the last months of this year, or 2022, the latest.

The future will depend much on the development of the pandemic and on the following economic recovery, but whatever happens, expect plugins to increase significantly its PEV share on the way.

There are two new faces on the Top 5, with the VW ID.4 debuting in 4th, with 10,318 units, its first five-digit score, while its (slightly) older brother, the ID.3, makes its first appearance this year, in #5.

In the podium, besides the Wuling Mini EV return to the top position, after a win in January, there an important mark concerning both Teslas, as last month the Tesla Model Y managed to beat the Model 3 for the first time ever, something that i believe will become the norm in a not too distant future.

Just below this Top 5, we have the Li Xiang One showing up in #7, becoming April's Best Selling PHEV, ahead of two Volvos, the XC60 PHEV (5,005 units), and the Volvo XC40 PHEV (4,589), highlighting the good moment of the Swedish maker.

On the YTD table, everything remained stable on the Top 5, but below it, balance is the word, with less than 4,000 units separating the #6 Nissan Leaf from the #20 Chevrolet Bolt.

But despite this balance, there weren't much position changes to the table, with the most important being the Li Xiang One jumping to 12th, overcoming the BMW 530e/Le, that had a slow month, with the Chinese startup model now joining the full size category podium, while being just 481 units from the runner-up Audi e-Tron, so we might see the Chinese EREV overcome the big Audi soon and have a 1-2 Chinese leadership in the full size category, as the category leader, the #4 BYD Han EV, seems unattainable.

Volkswagen had a great month, with the ID.4 joining the table in #13, thus making 15 BEVs in the Top 20, allowing the crossover to surpass for the first time its ID.3 relative, that despite this, had a positive month, with the German hatchback jumping 3 spots, to #13, with Volkswagen EV in recovery mode, the Nissan Leaf Best Seller status in the compact class is going to be tested soon, as both hatchbacks are now separated by less than 2,000 units.

Outside the Top 20, there are a few interesting developments, the most surprising of all being the rise to #22 of the Toyota Prius PHEV, that thanks to 4,715 units in April, its best score in over 3 years, allowed the Japanese hatchback to be just 1,500 units behind the #20 Chevrolet Bolt, and highlighting Toyota's good month, the RAV4 PHEV had its best score so far, with 3,996 units, so don't rule out Toyota from the 2021 Best Sellers table just yet...

Speaking of records, right now there are two models scoring consecutive record performances, with the BYD Qin Plus PHEV registering 3,603 units last month, it's 3rd record score in a row, while Hozon's Neta V had 3,846 units last month, it's second consecutive record, expect the BYD model to continue ramping up production (up to five-digits?), while one wonders if the startup Hozon has finally struck gold, with its small crossover.

Manufacturers: Volkswagen climbs to #3

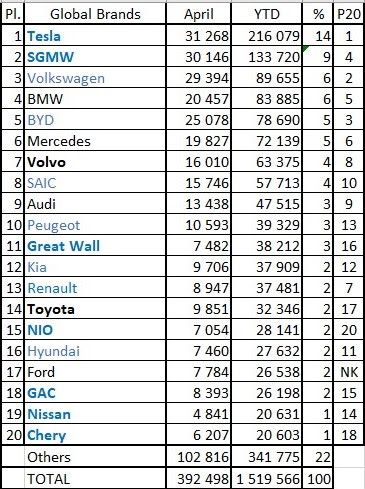

In April, Tesla took the monthly trophy, it's third in a row, but the top three brands were close, with only 1,874 units separating the #1 Tesla from the #3 Volkswagen.

Speaking of Volkswagen, the German brand has surpassed BMW in April and joined the podium, in 3rd, thanks to the good performances of the ID.3 and ID.4.

By the look of things, do not expect BMW to hold on to the 4th position for long, as #5 BYD is recovering momentum and might already surpass it in May, leaving the Bavarian brand withing sight of the rising #6 Mercedes, that has won 3% share YoY, while in the same period, BMW dropped from 7% in April 2020, to the current 6%.

Peugeot joined the Top 10, while Kia also climbed one position, in this case to 12th, but with just 2,000 units separating the #10 Peugeot from the #13, anything can happen.

On the lower half of the table, #18 GAC had its best score in 16 months, thanks to the landing of the new Aion Y.

Outside the Top 20, a reference to the 6,062 registrations of Skoda, but the brands closer to join the table are the #21 Xpeng (18,436 units) and #22 Li Xiang (18,118).

By OEM, Tesla (14%, down 2%) is ahead, followed by SAIC (13%), with the Volkswagen Group (13%, up 1%) closing in on both.