BEVs Jump 42% and Reach 23% Market Share!

Makings EVs Great Again — EV Share Jumps to 33% in Europe!

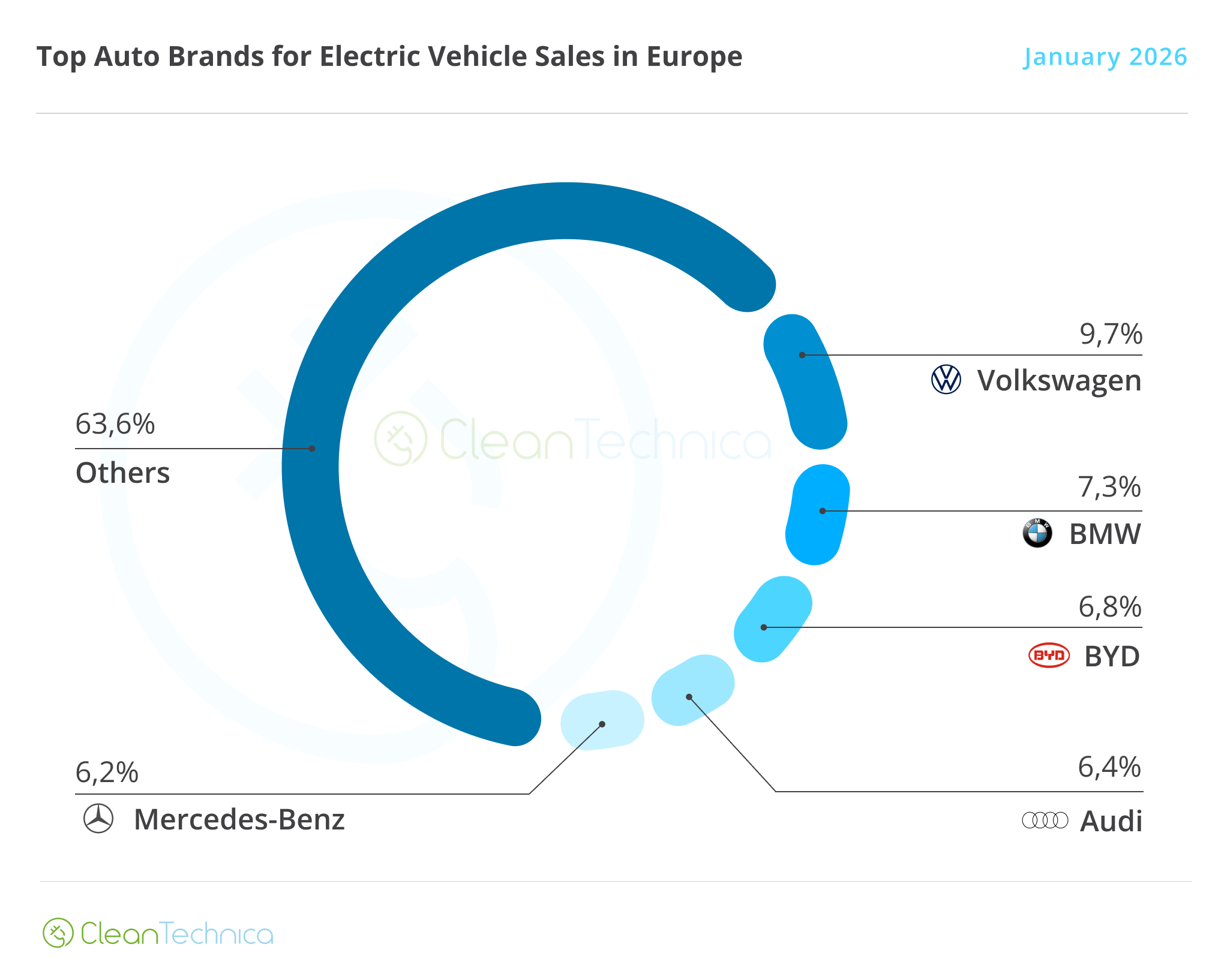

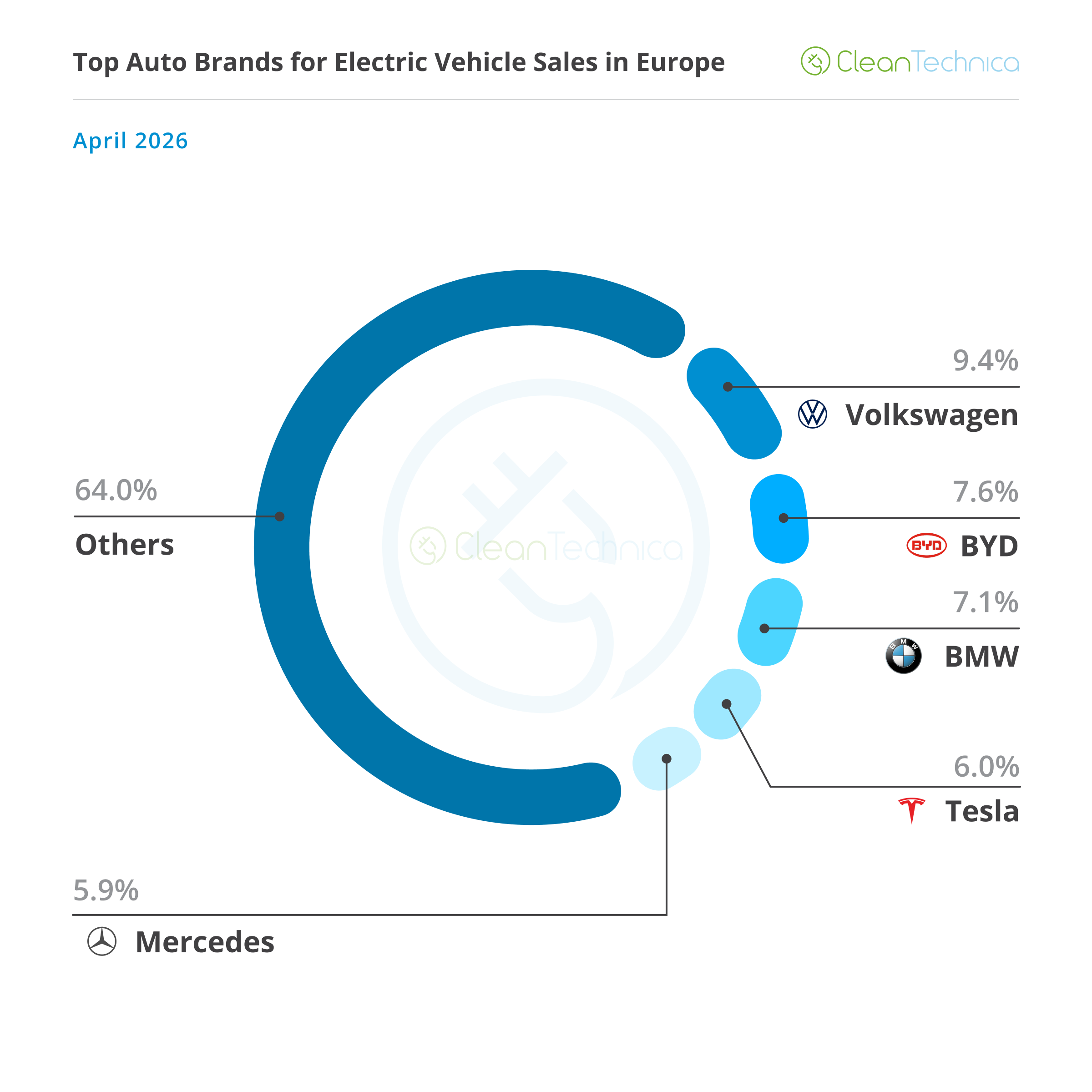

Brands Ranking - BYD rises and Mercedes (re)joins the Top 5

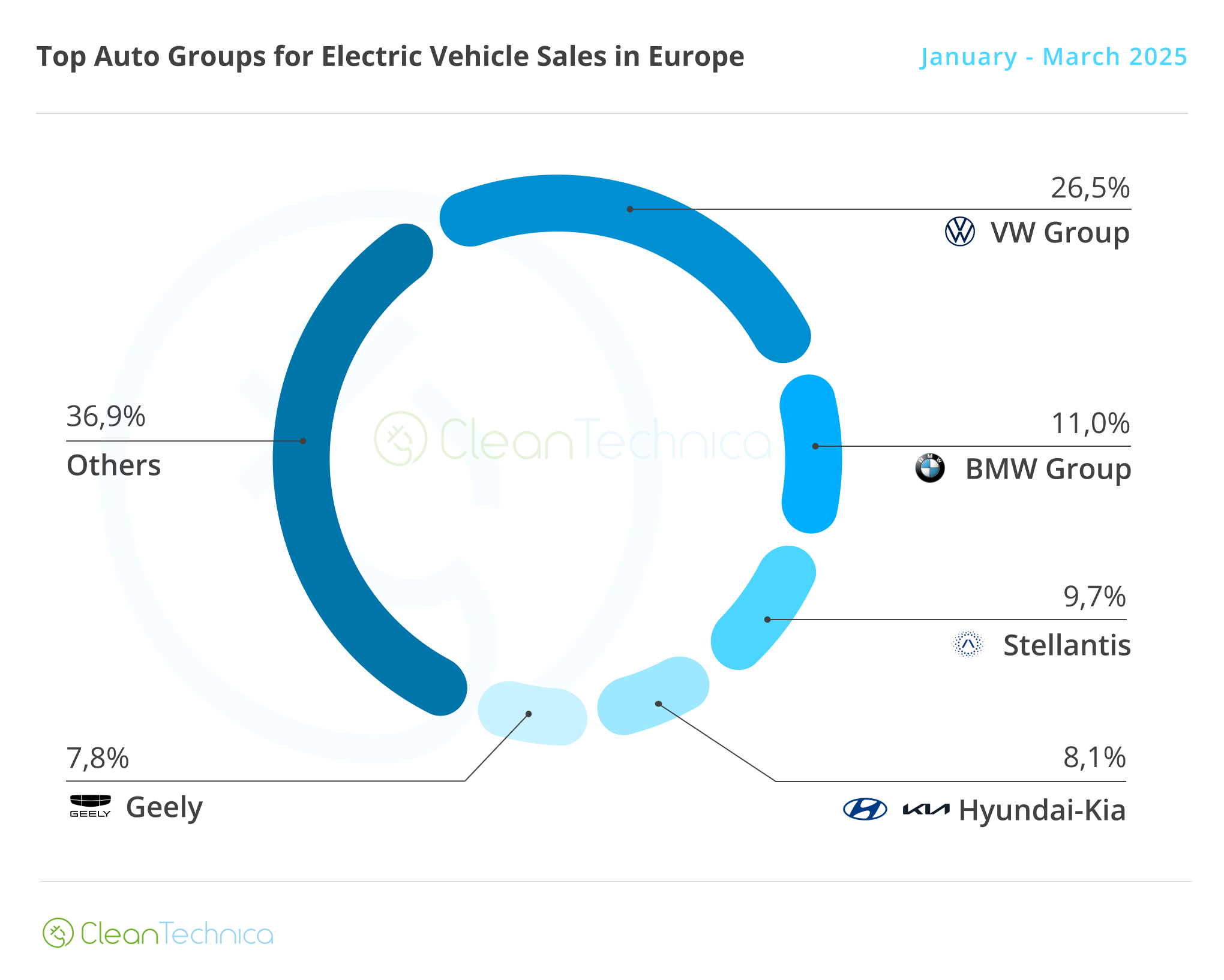

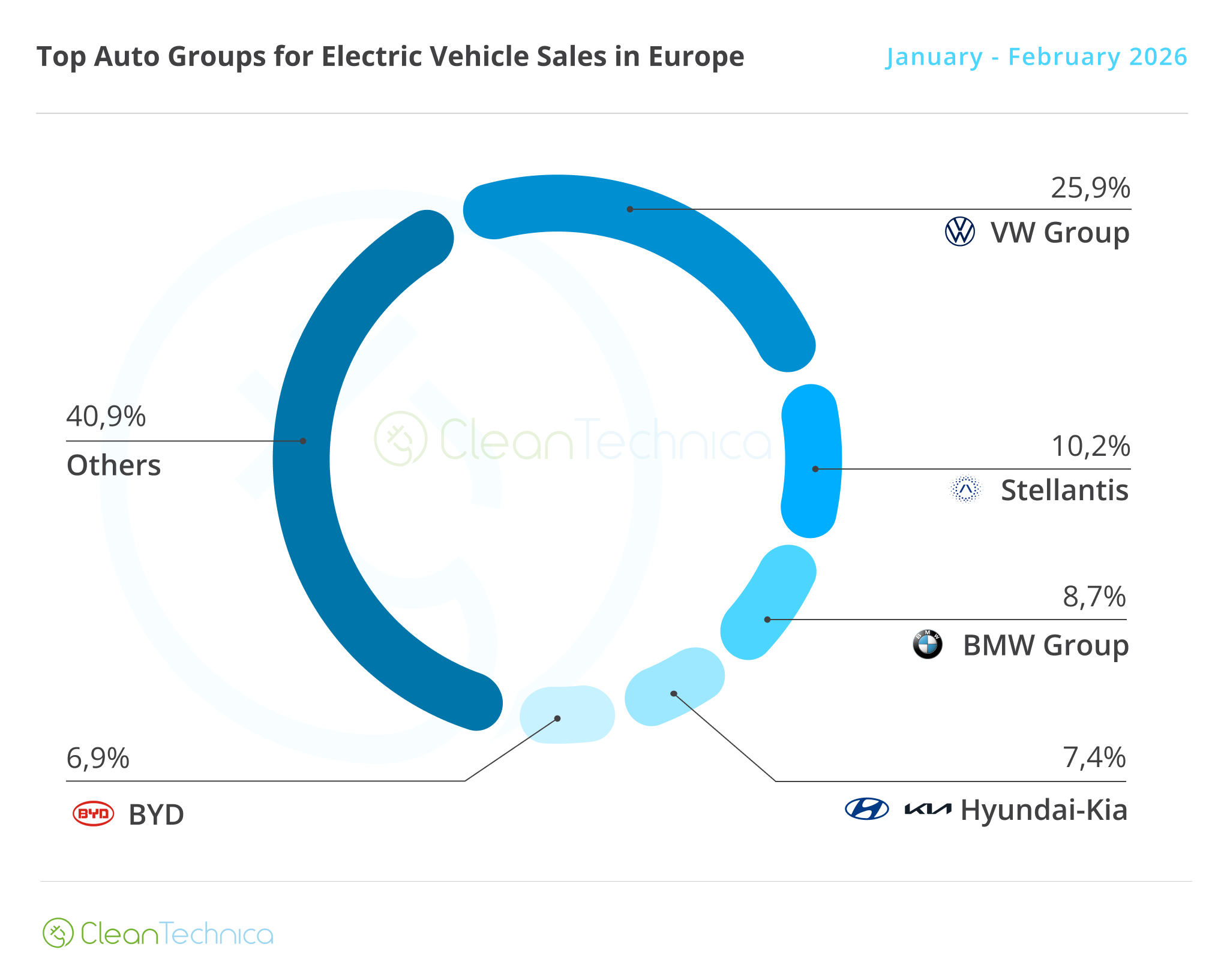

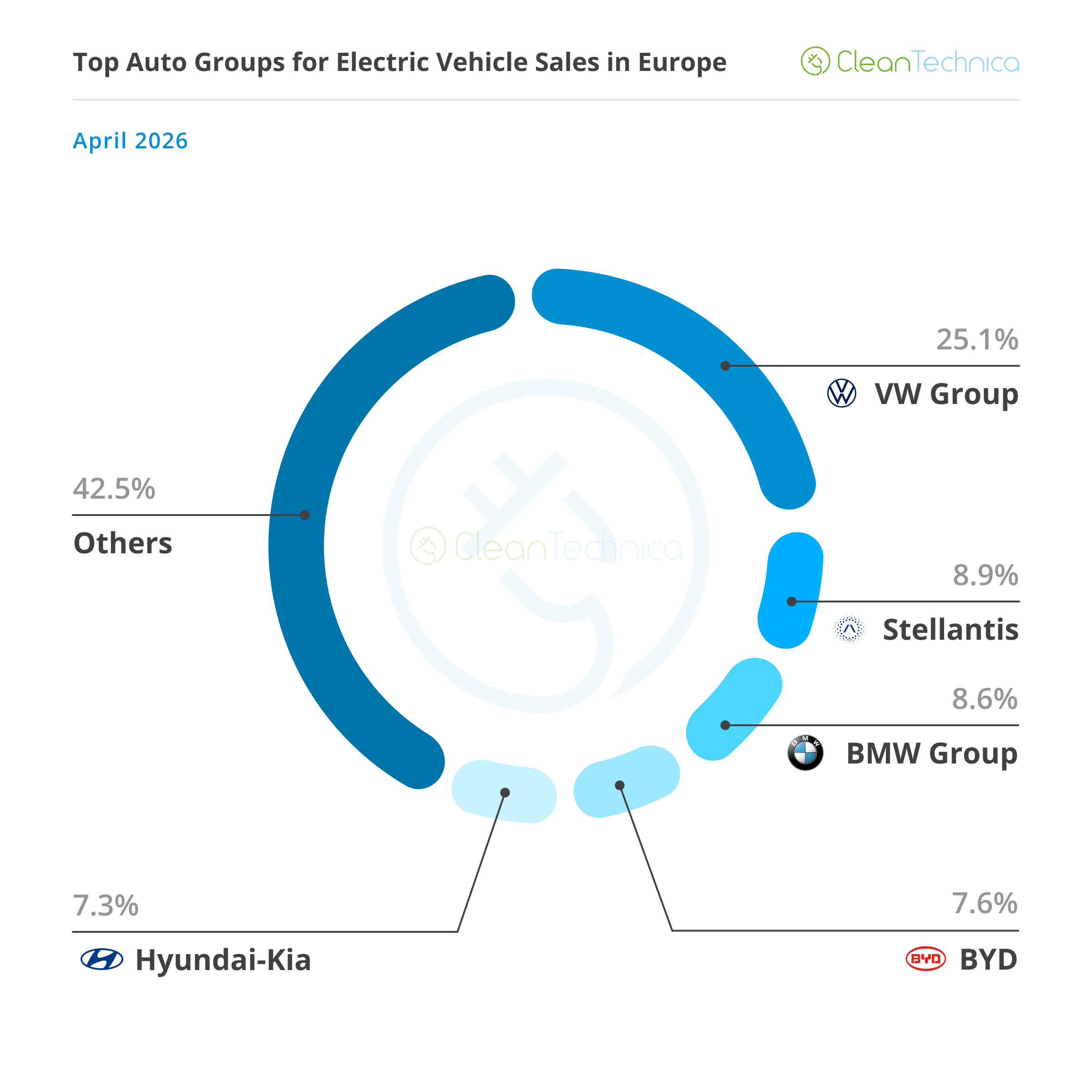

OEMs Ranking - BYD rises, Stellantis sinks

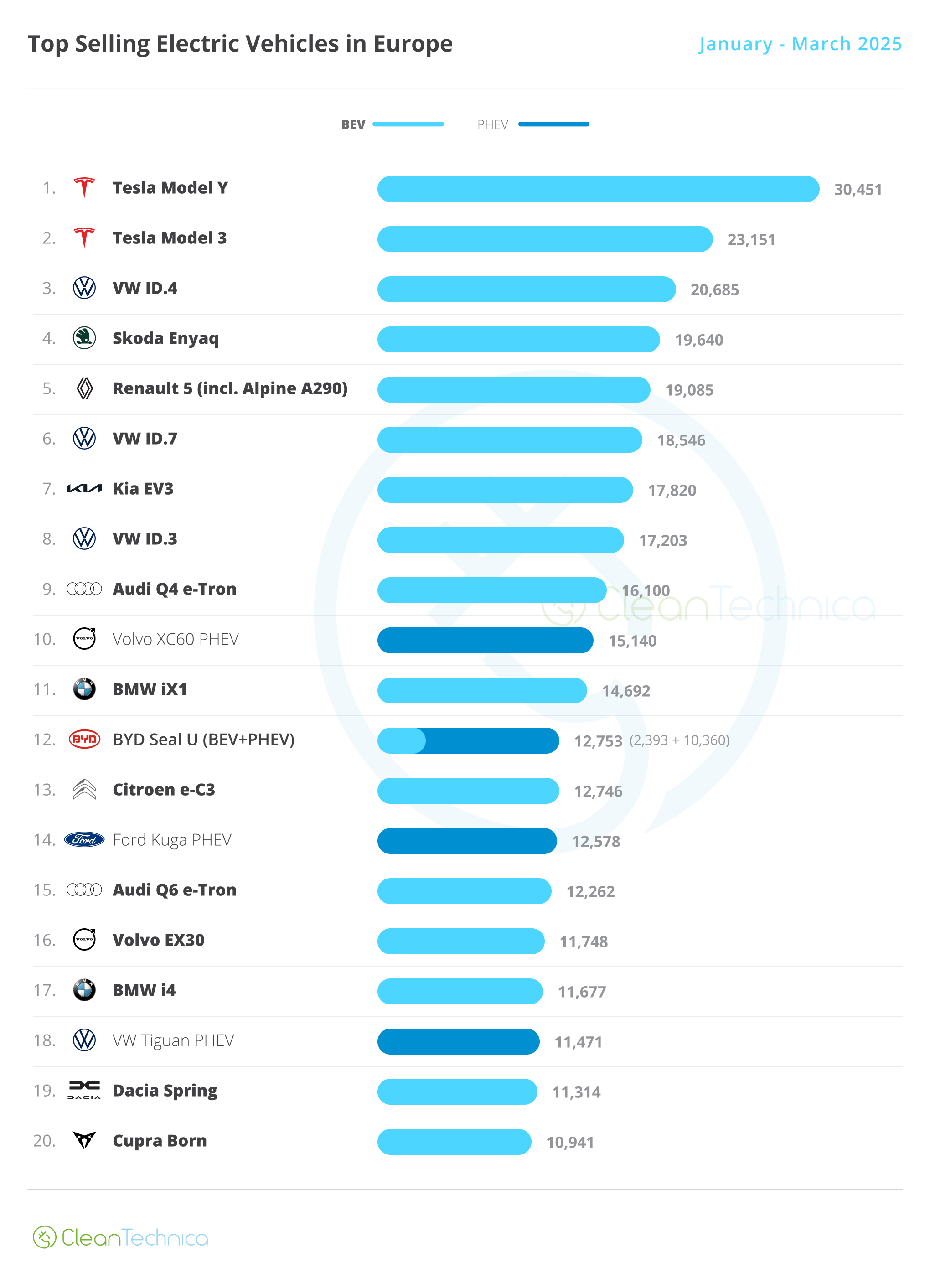

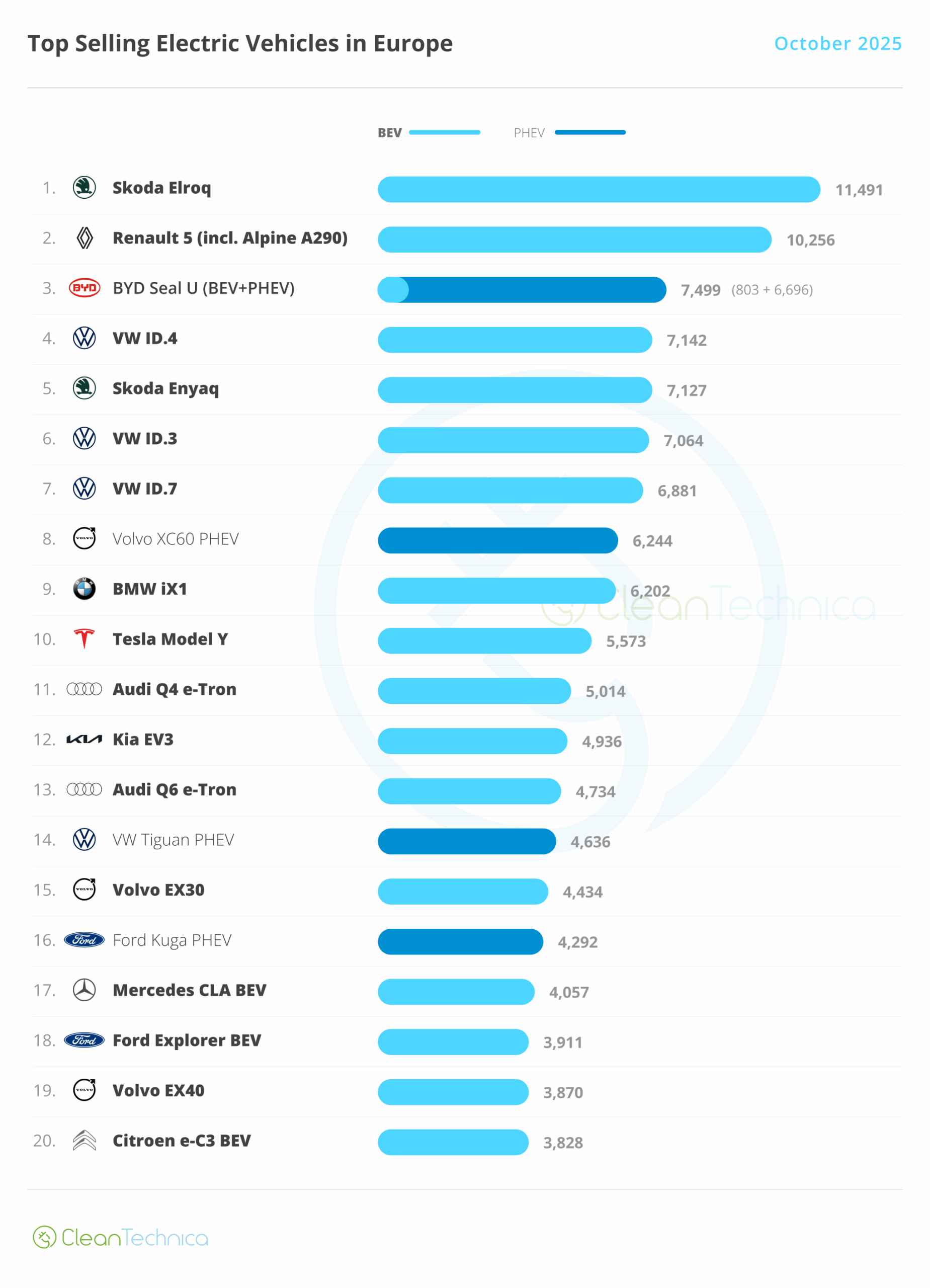

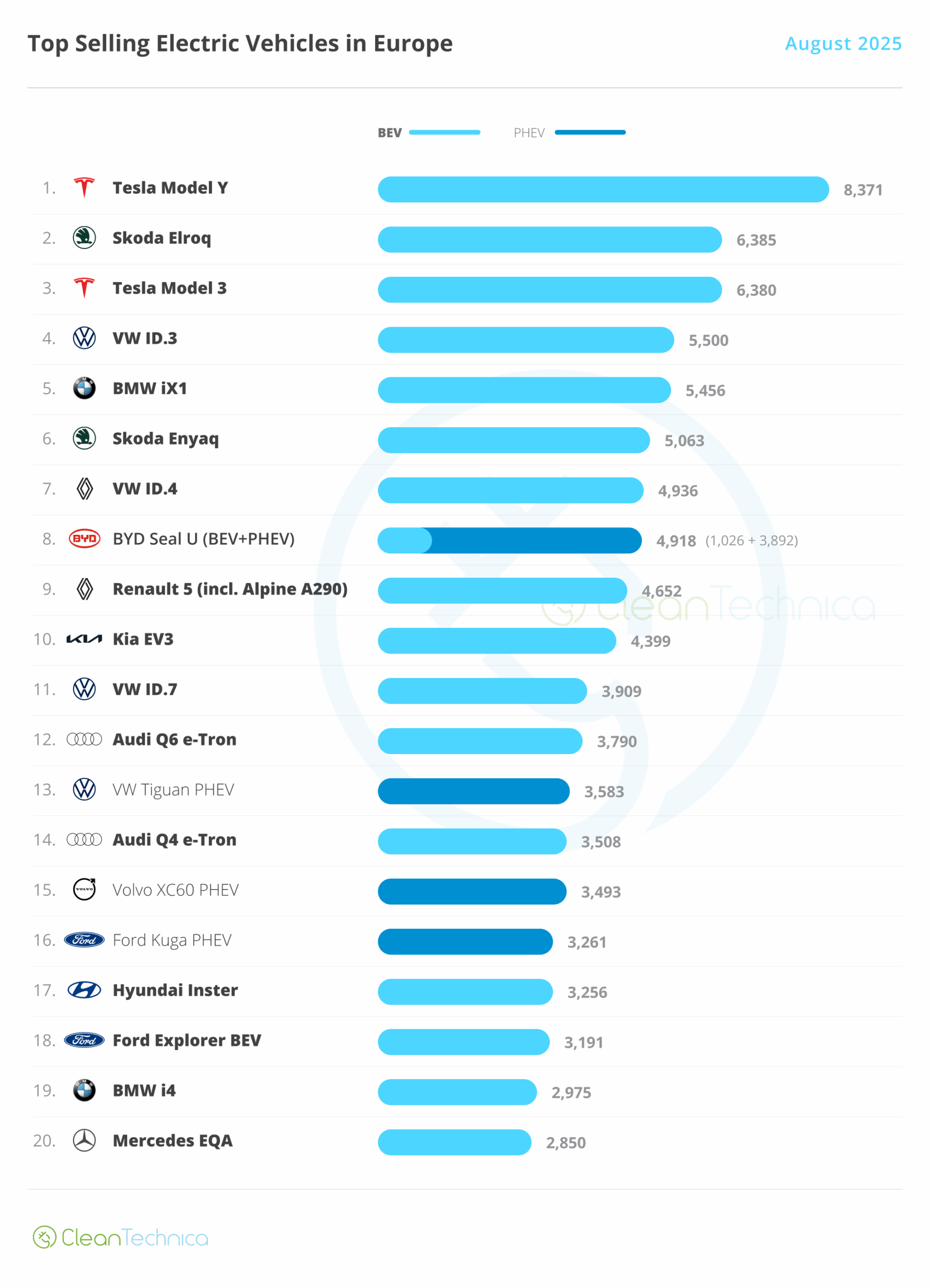

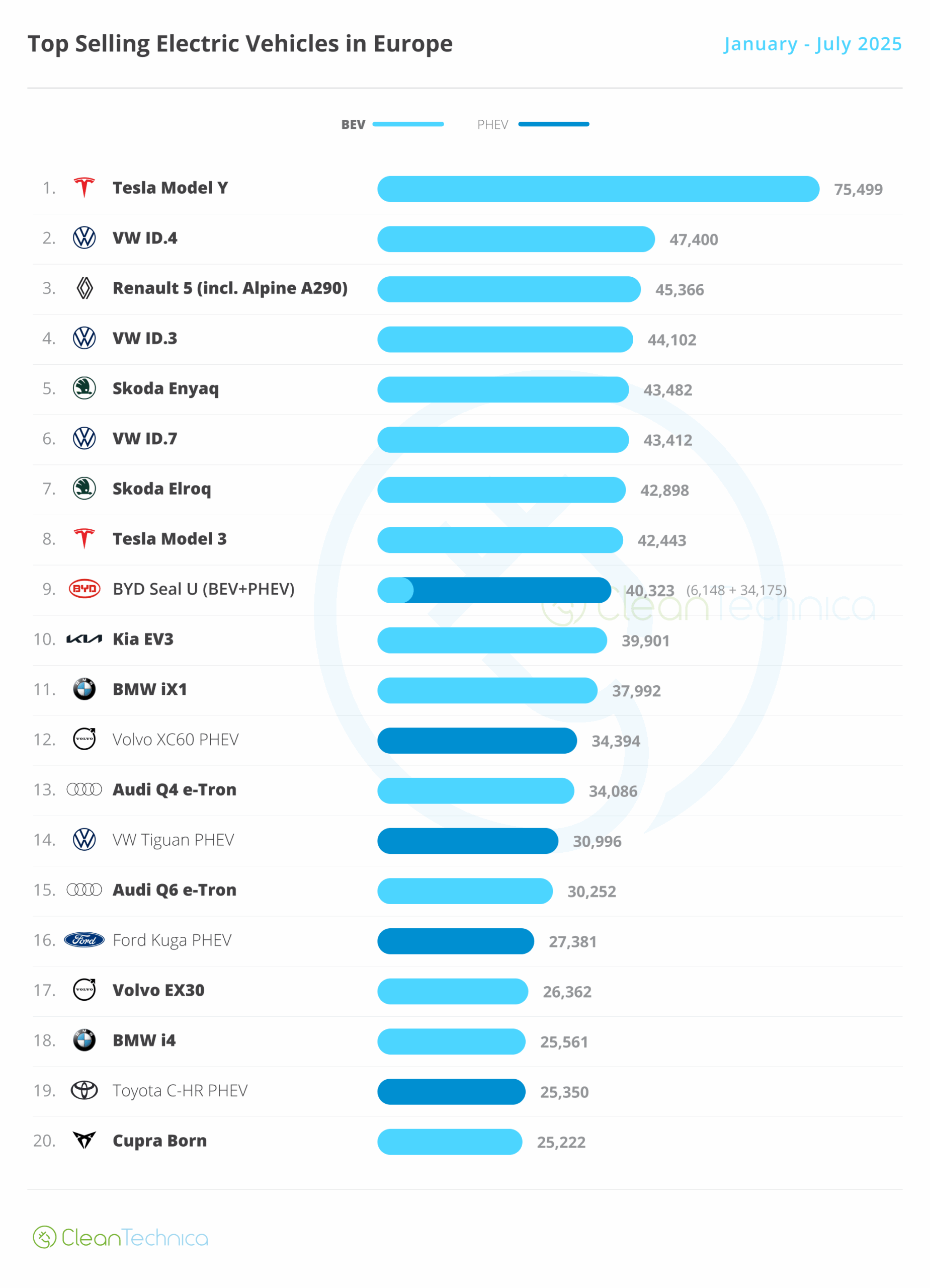

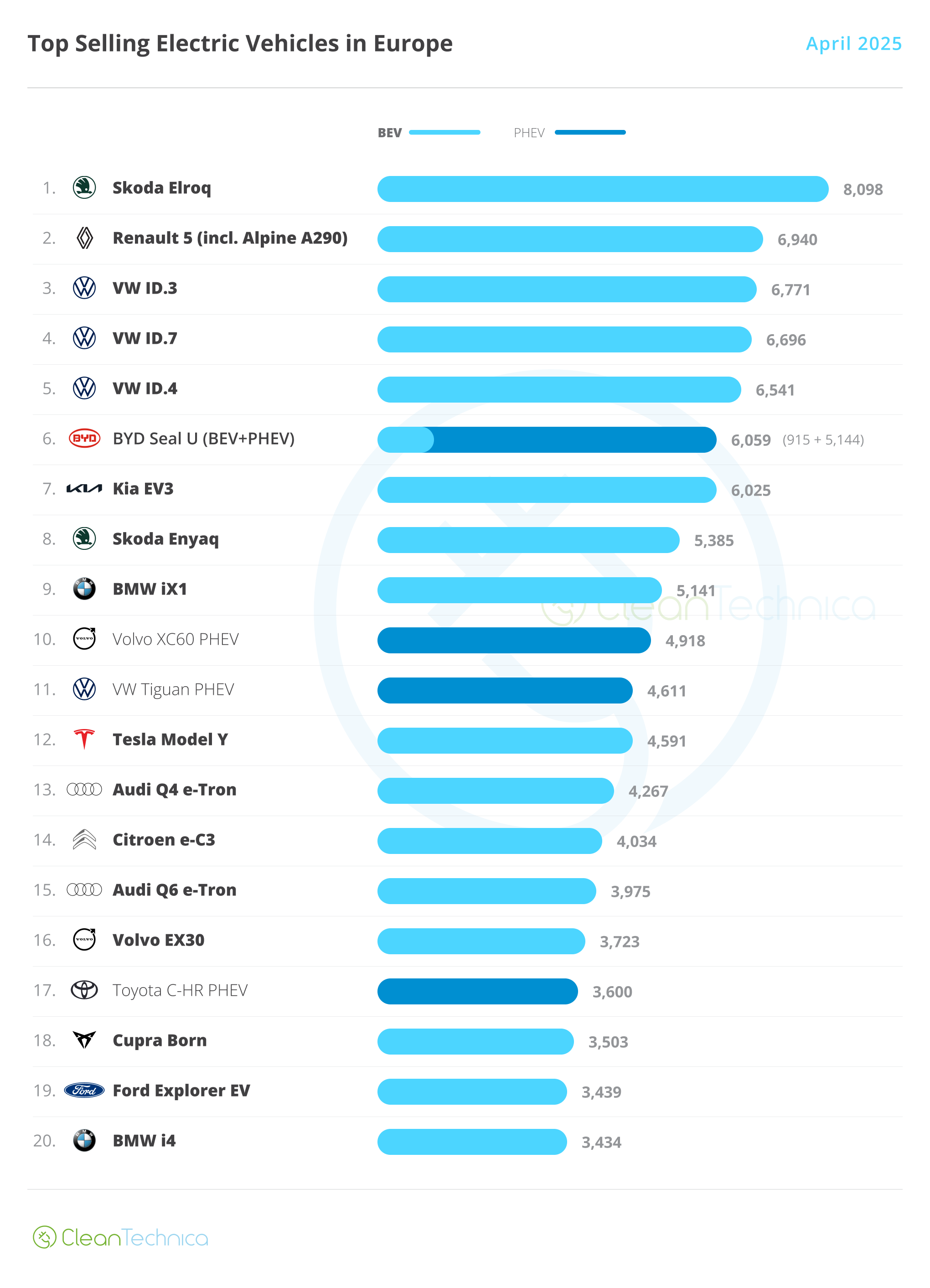

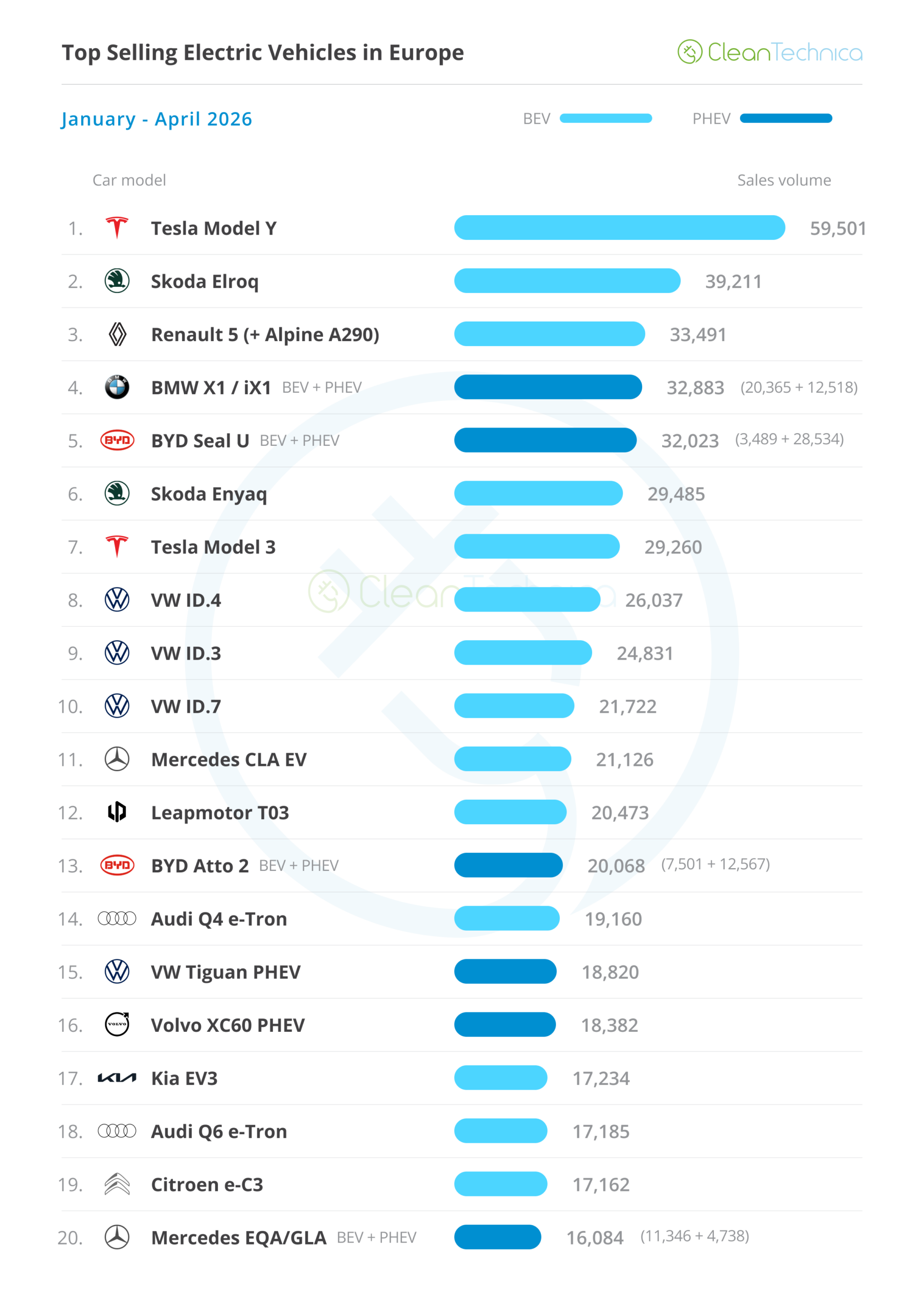

Electric and plug-in hybrid car sales rankings

Regarding OEMs, the VW Group consolidated its leadership, BMW retained the 2nd spot, while a sliding Stellantis replaced a crashing Tesla on the 3rd spot. Will Geely replace Stellantis in 2026?

It was the second best month ever in Europe - 26% PEV share in March, 25% YTD