My bets for the 2025 top 5 OEMs:

xEV

- BYD

- Geely

- Tesla

- SAIC

- VW Group

BEV

- BYD

- Tesla

- Geely

- SAIC

- VW Group

What are your bets?

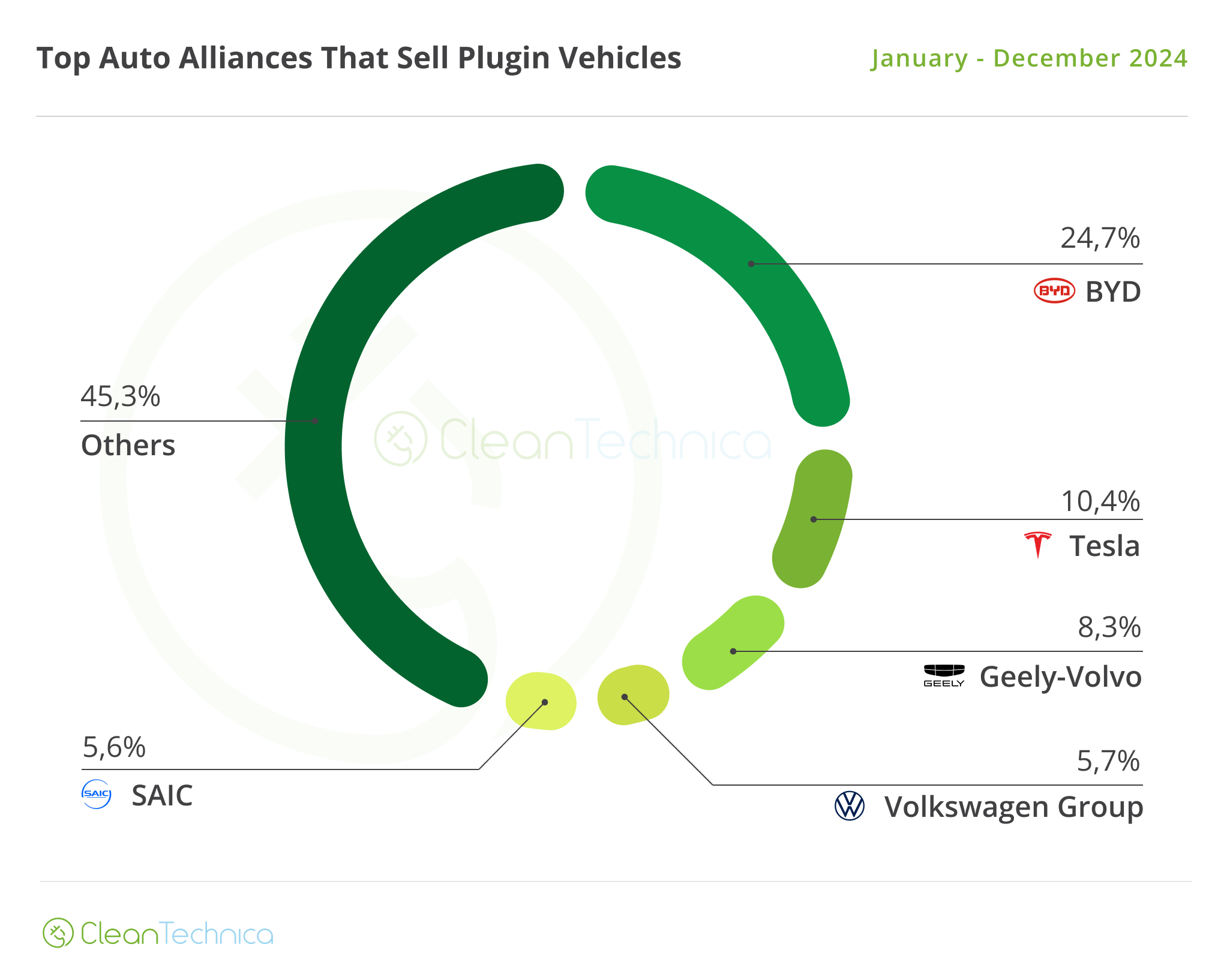

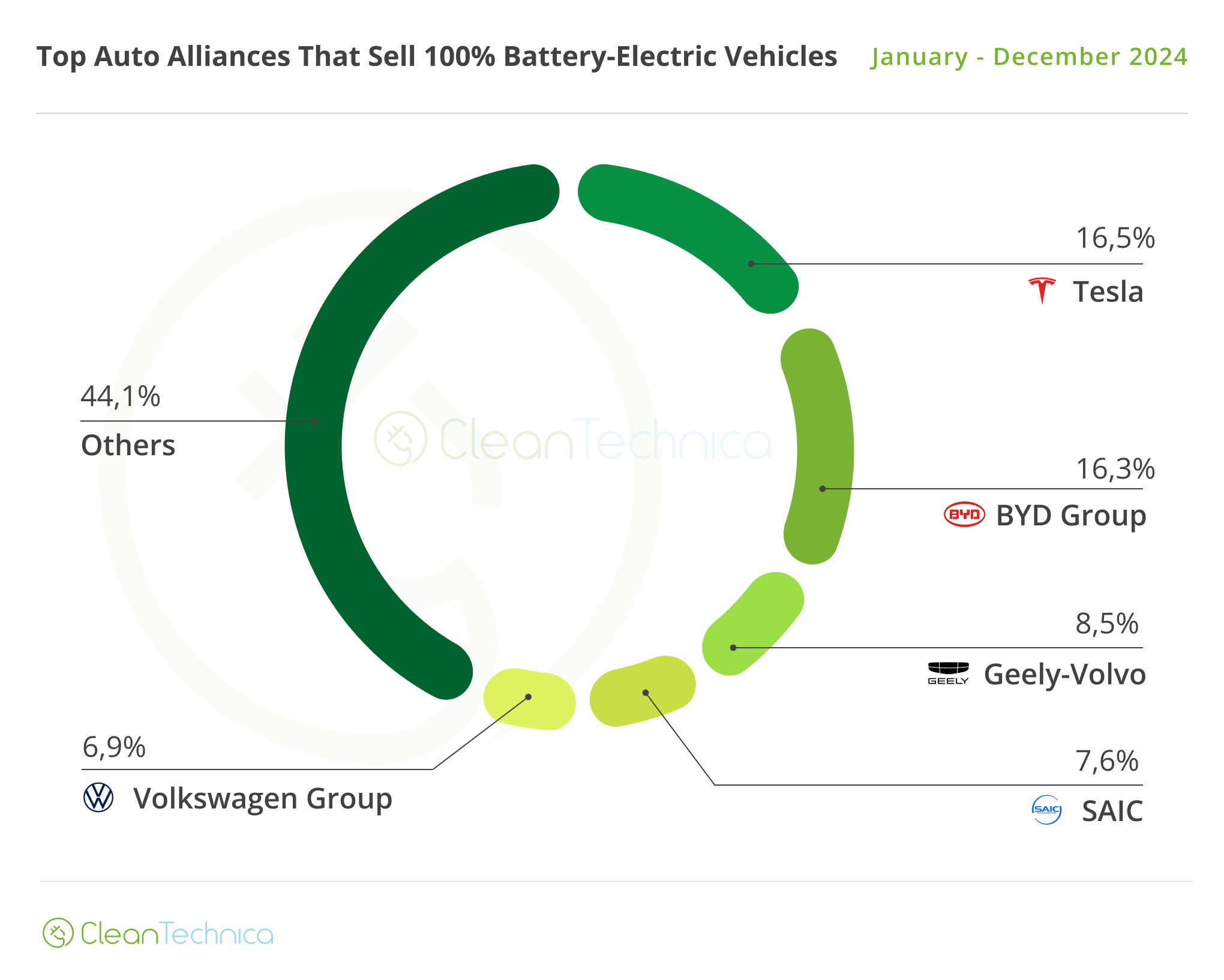

Electric and plug-in hybrid car sales rankings

My bets for the 2025 top 5 OEMs:

xEV

BEV

What are your bets?

Rising BYD was the best selling EV maker in 2024

Best Selling legacy brand was BMW(!), in 5th, behind a rising #4 Geely

Looking at 2025, expect BYD to continue rising, Tesla to drop below the 10% mark, but retain the 2nd position, while Geely will go all out and try displace Wuling from the 3rd spot.

Considering the difference in firepower between both brands, not only regarding lineup, but also number of markets where both are present, it is likely that Geely will end the year in 3rd, this being the podium by the end of the year:

1. BYD

2. Tesla

3. Geely

A final note on Toyota, the legacy brand that most progressed in the top 20(!)

Comparing 2023 with 2024, the Japanese car maker jumped from #19 to #14, growing its market share by almost 50%(!), to 1.5%.

And with Toyota apparently being serious in making the new Urban Cruiser crossover a success, it should continue climbing in the table.

(Well, it was about time for Toyota to take the EV game seriously)

Looking at the Q1 2021 sales by Automotive Group, we have:

Looking at the 2020 sales by Automotive Group, we have:

There are only 2 OEMs that have surpassed that milestone, both happening this year:

Tesla got there around last April;

The Renault-Nissan Alliance reached the 1 million mark a month later, in May.

And who will be next?

Well, BYD and the VW Group are the main candidates, but both shouldn't be able to get there this year, but expect at least one of them to get there by Q1 2021.

If the plugin market as a whole grew 76% in July, in that period, some OEMs grew above average, so this post mentions who was in the fast lane, last month.

Average in July: +76% growth YoY.

Fastest growers:

#1 - PSA (+2.477% YoY);

#2 - Ford Group (628%);

#3 - Volvo Group (360%);

#4 - Daimler (351%);

#5 - VW Group (268%).

For further information, Hyundai-Kia was up 91% YoY and Tesla 49%.

Of course, this simplistic approach is skewed to help smaller OEMs, because if you sold 2 units instead of 1, it means a 100% growth, hence the success of the Top 3 OEMs.

So the best approach is to look at total volume, and here, the OEMs that grew more regarding July 2019, volume wise, are:

#1 - VW Group (24.909);

#2 - Daimler (11.534);

#3 - Tesla (10.816).

If the first spot of the Volkswagen Group can surprise some, if you think about the sales uptick that the German Conglomerate had in the past year, it should come as no surprise, as the sheer scale of the Group means that a couple percent of electrification translates into several thousand units.

The real surprise, including for me, is the second place of the Daimler Group (Mercedes + Smart), that just managed to overcome Tesla, mostly thanks to a surge in sales of the Smart brand, as well as the ramp up of the Mercedes PHEVs and even the EQC has started to be delivered in decent volumes.

Finally, Tesla. And a disclaimer. Because this is the first month of the quarter, one shouldn't read too much into these numbers, as the previous normal quarters (Q4 2019; Q1 2020) saw Tesla increasing the seasonality of sales, with lower than average numbers in the first two months, and then an end of quarter month with higher than usual deliveries, so i wouldn't be surprised if the same happened again this quarter.